The 3 Golden Rules to Real Estate Investing

Real estate investing can be a powerful avenue for building wealth, but knowing how to analyze potential deals is crucial. In this article, we'll explore the three essential rules that seasoned investors use to evaluate rental properties and flips effectively.

Real estate investing can be a powerful avenue for building wealth, but knowing how to analyze potential deals is crucial. In this article, we'll explore the three essential rules that seasoned investors use to evaluate rental properties and flips effectively.

Introduction to Real Estate Investing

Real estate investing is one of the most effective ways that an average person can achieve true wealth in their lifetime. When done properly, it offers a reliable path to financial independence. However, the key to success in real estate investing lies in the ability to analyze deals accurately and efficiently. Knowing how to crunch the numbers is essential.

Experienced real estate investors have devised a few simple rules of thumb to quickly evaluate whether a property is worth further consideration. These rules help determine if a property has potential and if deeper analysis is warranted. Mastering these rules can save time and help avoid costly mistakes.

In this guide, we will explore the three most effective rules of thumb for real estate investing. By understanding and applying these rules, you can make more informed decisions and increase your chances of success in the real estate market.

Understanding the 1% Rule

The first rule we're going to discuss is the 1% rule. This rule is a quick and straightforward way to assess whether a property will generate sufficient rental income. To apply the 1% rule, you take the expected monthly rental income and divide it by the value of the house. Ideally, this ratio should be 1% or greater.

If the result is 1% or more, the property is likely to be a good investment. Conversely, if the ratio is below 1%, it might not be the best choice. The 1% rule helps investors quickly filter properties and focus on those with the potential for positive cash flow.

Applying the 1% Rule

For example, if a home is worth $200,000, you would want to get at least $2,000 per month in rent for that property. If the monthly rent meets or exceeds this amount, the property passes the 1% rule.

However, it's important to note that not all homes make good rental properties. The demand for rentals can vary significantly by location. In some areas, there may be a high demand for rentals, leading to a higher rent-to-home value ratio. In other areas, the demand may be low, resulting in a lower ratio.

Challenges in the Current Market

In today's market, finding properties on the MLS (Multiple Listing Service) that meet the 1% rule can be challenging. Nonetheless, the 1% rule remains a valuable benchmark for evaluating potential investments. Even if a property doesn't meet the 1% rule exactly, it can still be a good deal if it comes close.

For instance, a property that rents for 0.9% or 0.8% of its value may still be a worthwhile investment. The closer you can get to the 1% rule, the better your chances of achieving positive cash flow.

The Importance of the 50% Rule

The 50% rule is crucial for anyone venturing into rental property investments. This rule states that, on average, 50% of your rental income will go towards operating expenses. These expenses include property taxes, insurance, repairs, and maintenance, but exclude the mortgage payment.

Understanding Operating Expenses

Operating expenses can vary greatly depending on the property and its location. However, the 50% rule provides a useful baseline. By assuming that half of your rental income will be used for these expenses, you can better estimate the profitability of your investment.

- Property Taxes: These are mandatory payments to local governments based on the assessed value of the property.

- Insurance: This protects your investment from potential risks such as fire, theft, or natural disasters.

- Repairs and Maintenance: These costs cover the upkeep of the property, ensuring it remains livable and attractive to tenants.

Applying the 50% Rule

Let's say you rent out a property for $2,000 per month. According to the 50% rule, $1,000 of that income will go towards operating expenses. This leaves you with $1,000 to cover your mortgage and any desired profit.

For instance, if you aim to make a $100 profit each month, your mortgage payment should not exceed $900. By understanding this, you can determine the maximum purchase price for a rental property to ensure it remains a profitable investment.

Further Analysis

The 50% rule is a rough estimate and should be used as a starting point. If a property meets this rule, it's worth conducting a more detailed analysis. Look up actual property taxes, get insurance quotes, and estimate repair costs based on the property's age and condition.

By doing so, you can make a more informed decision about whether the property is a sound investment. The 50% rule helps you quickly identify properties that might be worth deeper investigation, saving you time and effort in the long run.

Applying the 70% Rule for Fix and Flips

When it comes to fix and flips, the 70% rule is an essential guideline. This rule helps investors determine the maximum price they should pay for a property to ensure a profitable flip. According to the 70% rule, you should only pay 70% of the property's after repair value (ARV) minus the estimated repair costs.

Calculating the ARV

The ARV is the price at which you expect to sell the property after all repairs and renovations are complete. To apply the 70% rule, you first need to estimate this value accurately. Look at comparable properties in the area that have recently sold to get a realistic idea of the ARV.

For example, if you believe a property will sell for $300,000 after repairs, you would calculate 70% of this value, which is $210,000.

Estimating Repair Costs

The next step is to estimate the repair costs. These costs can vary significantly depending on the property's condition and the extent of the renovations needed. Common repair costs include structural repairs, cosmetic updates, and any necessary improvements to meet current building codes.

Let's say you estimate the repair costs to be $50,000. According to the 70% rule, you would subtract these repair costs from the 70% ARV. In this case, $210,000 - $50,000 = $160,000. This means the maximum purchase price for this property should be $160,000 to ensure a profitable flip.

Understanding Operating Expenses

The 70% rule also accounts for various operating expenses associated with flipping a property. These expenses include closing costs, real estate agent commissions, holding costs (such as utilities and property taxes during the renovation period), and other miscellaneous costs.

By lumping these expenses together, the 70% rule simplifies the calculation process. It ensures that you only need to focus on two main numbers: the ARV and the repair costs, making it easier to determine whether a property is a good investment.

Limitations of the 70% Rule

While the 70% rule is a valuable tool, it has its limitations. It works best for properties within the average home value range in the U.S., typically around $300,000 to $500,000. For properties at the extreme ends of the price spectrum, the rule may not be as effective.

For high-end properties worth $1 million or more, the 70% rule might result in an unrealistically low purchase price. Similarly, for lower-end properties valued at $50,000 to $70,000, the rule might not account for the fixed costs involved in flipping, leading to an overestimation of profitability.

Despite these limitations, the 70% rule remains a valuable guideline for most fix and flip investments. If a property meets this rule, it indicates potential profitability and warrants a more detailed analysis to confirm the numbers.

By applying the 70% rule, you can make more informed decisions, minimize risks, and increase your chances of success in the fix and flip market. With careful analysis and adherence to these guidelines, real estate investing can be a rewarding and profitable venture.

Analyzing Rental Properties Effectively

When diving into real estate investing, one of the most critical skills to develop is the ability to analyze rental properties effectively. This involves understanding and utilizing various metrics and rules of thumb to quickly determine whether a property is worth pursuing. Here, we'll delve into the essential aspects of analyzing rental properties to ensure you make informed and profitable citizenship by investment investments.

Key Metrics to Consider

Several key metrics can help you gauge the potential of a rental property. These include:

- Gross Rent Multiplier (GRM): This is calculated by dividing the property price by the annual rental income. A lower GRM indicates a better investment.

- Capitalization Rate (Cap Rate): This is the net operating income (NOI) divided by the property price. A higher cap rate typically means a better return on investment.

- Cash on Cash Return: This measures the annual return on the actual cash invested. It's calculated by dividing the annual pre-tax cash flow by the total cash invested.

Understanding the Market

Knowing the local market is crucial when analyzing rental properties. This includes understanding the demand for rentals, the average rental rates, and the local economic conditions. A property in a high-demand area with stable or growing economic conditions is more likely to be a profitable investment.

Research local rental listings and talk to property managers to get a sense of the rental market. Look for trends in rental rates and vacancy rates to gauge the property's potential for consistent rental income.

Evaluating Property Condition

The condition of the property is another vital factor to consider. A property in poor condition may require significant repairs and maintenance, which can eat into your profits. Conduct a thorough inspection to identify any potential issues and estimate the repair costs accurately.

Consider hiring a professional inspector to assess the property's condition. This can help you avoid unexpected expenses and ensure you have a clear understanding of the property's needs.

Location, Location, Location

The location of a rental property can significantly impact its profitability. Properties in desirable neighborhoods with good schools, amenities, and low crime rates tend to attract higher rental rates and more reliable tenants. Conversely, properties in less desirable areas may struggle to attract tenants and command lower rents.

Research the neighborhood thoroughly before making a purchase. Look at crime rates, school ratings, proximity to amenities, and future development plans. These factors can all influence the property's long-term value and rental potential.

Finding the Right Investment Strategy

Choosing the right investment strategy is essential for achieving success in real estate. Different strategies can yield varying returns and involve different levels of risk, effort, and expertise. For investors who need access to funds for renovations, deposits, or other property-related expenses, understanding personal loans payments can also play an important role in effective financial planning. Here, we'll explore some popular real estate investment strategies to help you find the one that aligns with your goals and resources.

Buy and Hold

The buy and hold strategy involves purchasing rental properties and holding onto them for an extended period. This approach focuses on generating steady rental income and benefiting from property appreciation over time. It's a popular strategy for building long-term wealth.

Buy and hold investors typically look for properties in stable or growing markets with good rental demand. They aim to achieve positive cash flow, where the rental income exceeds the property's expenses, including the mortgage, taxes, insurance, and maintenance.

Fix and Flip

Fix and flip is a more active investment strategy that involves buying properties in need of renovation, making improvements, and then selling them for a profit. This strategy can yield significant returns but also involves higher risks and requires more hands-on involvement.

Successful fix and flip investors need to have a keen eye for properties with potential, strong project management skills, and a good understanding of the local market. They must also be able to accurately estimate renovation costs and timelines to ensure profitability.

Wholesaling

Wholesaling involves finding properties at discounted prices, putting them under contract, and then selling the contract to another investor for a fee. This strategy requires little to no capital investment and can be a good way to enter the real estate market without owning property.

Wholesalers need strong negotiation skills and a good network of buyers and sellers. They must also be able to identify properties with potential and act quickly to secure deals.

House Hacking

House hacking is a strategy where the investor lives in one part of a property while renting out the other parts. This can involve renting out rooms in a single-family home, living in one unit of a multi-family property, or even renting out a basement or garage apartment.

This strategy allows investors to reduce or eliminate their own housing costs while building equity and generating rental income. It's a popular approach for first-time investors looking to get started in real estate with minimal risk.

Commercial Real Estate

Investing in commercial real estate involves purchasing properties used for business purposes, such as office buildings, retail spaces, or industrial properties. This strategy can offer higher returns and longer lease terms compared to residential real estate, but it also involves higher risks and more complex management.

Commercial real estate investors need to understand the specific dynamics of the commercial market, including tenant needs, lease structures, and property management requirements. They must also be prepared for potentially longer vacancy periods between tenants.

Real Estate Investment Trusts (REITs)

For those looking to invest in real estate without the responsibilities of property ownership, Real Estate Investment Trusts (REITs) can be an attractive option. REITs are companies that own, operate, or finance income-producing real estate and allow investors to buy shares of the company.

Investing in REITs provides exposure to real estate assets with the liquidity and ease of trading stocks. It offers a way to diversify your investment portfolio and earn dividends from rental income without the need for direct property management.

Choosing Your Strategy

The right investment strategy depends on your financial goals, risk tolerance, and level of involvement you desire. Some investors prefer the steady, long-term returns of buy and hold, while others are drawn to the potential for quick profits with fix and flip.

Consider your available resources, including time, capital, and expertise, when selecting a strategy. It's also essential to stay informed about market trends and continuously educate yourself to adapt and succeed in the ever-changing real estate landscape.

By carefully analyzing rental properties and selecting the right investment strategy, you can maximize your chances of success in the real estate market. Whether you're looking for long-term wealth building or short-term gains, real estate offers a variety of opportunities to achieve your financial goals.

Homes for sale in Mesquite, Nevada

Thinking about a move to Mesquite?

Browse every active listing — Sun City 55+, golf-course homes, new construction and more — updated multiple times a day. Or talk to a local agent who knows the neighborhoods.

Keep reading

More from the blog

How to Create a Backyard You'll Actually Love

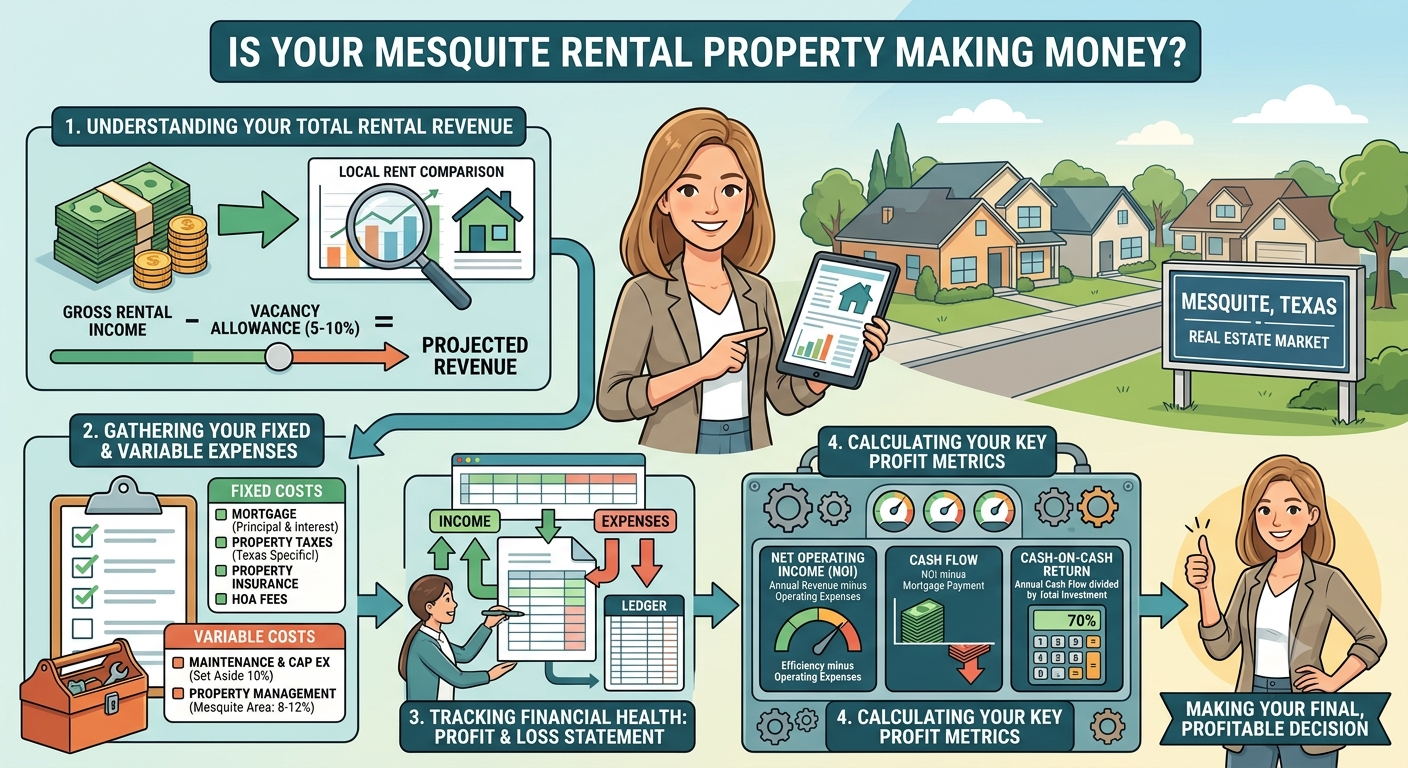

How to Calculate Whether a Mesquite Rental Property Is Profitable

Which Electric Chainsaw Works Best for Small Property Jobs?